An employee stock ownership plan (ESOP) is a type of qualified retirement plan that enables a business owner to gradually transfer ownership shares to employees. Moreover, establishing an ESOP sets up opportunities for the owner of a closely held business to cash out (in whole or in part) in the future, while keeping the company going for employees and the community.

An ESOP may be a good option for small-business owners who don’t plan to pass the reins to family members when they retire, but instead have loyal and capable managers who would be interested in taking over the company. In the meantime, an ownership mentality may enhance efficiency and productivity, because employees have a stake in the company’s long-term success.

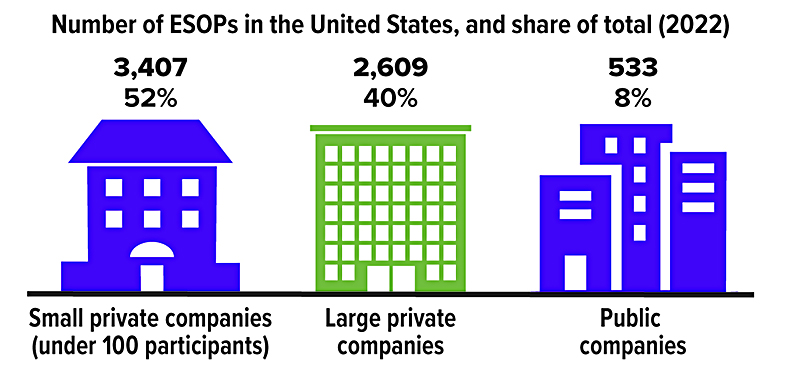

How ESOPs work

ESOPs are designed to invest their assets primarily in company stock rather than investing in the public markets. Annual cash contributions are made to the ESOP and used to purchase stock from the company, or the company may contribute the stock directly. In either case, the company can take a tax deduction for the value of each year’s contribution, while the cash stays with the company.

Unlike other retirement plans, ESOPs are permitted to borrow money to purchase company stock. The company then makes annual contributions to the ESOP in the amount equal to the ESOP’s principal and interest payments on the loan and uses the contributions to pay back that debt. The company’s contribution as a whole is deductible, so the interest and the principal on the loan are deductible as well.

With an ESOP, an employee never buys or holds the stock directly while still employed with the company. If an employee is terminated, retires, becomes disabled, or dies, the plan will distribute the vested shares of stock in the employee’s account.

ESOP participants are investing heavily in a single stock, and their investment is tied to the financial health of the business. If the company declines in value, the ESOP may also. Thus, an ESOP should generally be offered alongside a standard retirement plan [such as a (401k)] with more diversified investment options.

A tax-deferred exit

There may also be tax benefits for a retiring owner who sells a business to an ESOP. If the ESOP owns at least 30% of the company after the sale, the capital gains tax on the sale may be deferred by reinvesting the proceeds in domestic U.S. securities (“qualified replacement property”). No tax would be due until the replacement securities are sold. If they are held until death, a stepped-up basis may apply, and the original gain may never be taxed.

Business owners can defer taxes on the sale of business interests to an ESOP only if the shares were held for at least three years, and if the ESOP was established by a C corp (not an S corp). Among other conditions, stock bought by the ESOP may not be allocated to the seller or certain members of the seller’s family, or to any shareholder of the company establishing the ESOP who owns more than 25% of any class of company stock. If this rule is violated, the company would be subject to a 50% excise tax, and the person receiving the allocation would also be subject to tax consequences.

ESOPs can be complicated and costly to establish and maintain, but they offer significant tax advantages that make them worthwhile in certain situations. It would be wise to consult an attorney with experience in the formation and maintenance of qualified retirement plans to help evaluate whether an ESOP could be appropriate for your business.

All investing involves risk, including the possible loss of principal. There is no guarantee that any investing strategy will be successful. Diversification is a method used to help manage investment risk; it does not guarantee a profit or protect against investment loss.

IMPORTANT DISCLOSURES

ERB FINANCIAL offers Securities and Investment Advisory Services through Ashton Thomas Securities, LLC, member FINRA/SIPC,200 Canal View Blvd Rochester NY 14623 585-424-1234

Locally owned and operated since 1953

Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The information presented here is not specific to any individual’s personal circumstances.

To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances.

These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

This communication is strictly intended for individuals residing in the state(s) of NY. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2025.